What is florida definition of life insurance replacement – What is Florida’s definition of life insurance replacement? This comprehensive guide delves into the intricacies of replacing a life insurance policy within Florida’s legal framework. We’ll explore the specifics of the process, from the legal definitions and regulatory aspects to the consumer rights, agent responsibilities, and the financial implications involved.

Understanding the various types of replacement, including term and whole life, and the differences between similar and significantly different policies, is crucial for informed decision-making. This discussion will also clarify the consumer protections available and the responsibilities of agents in such transactions. We will also analyze the potential financial impacts and tax consequences, as well as how it might affect existing financial plans.

Definition of Life Insurance Replacement in Florida: What Is Florida Definition Of Life Insurance Replacement

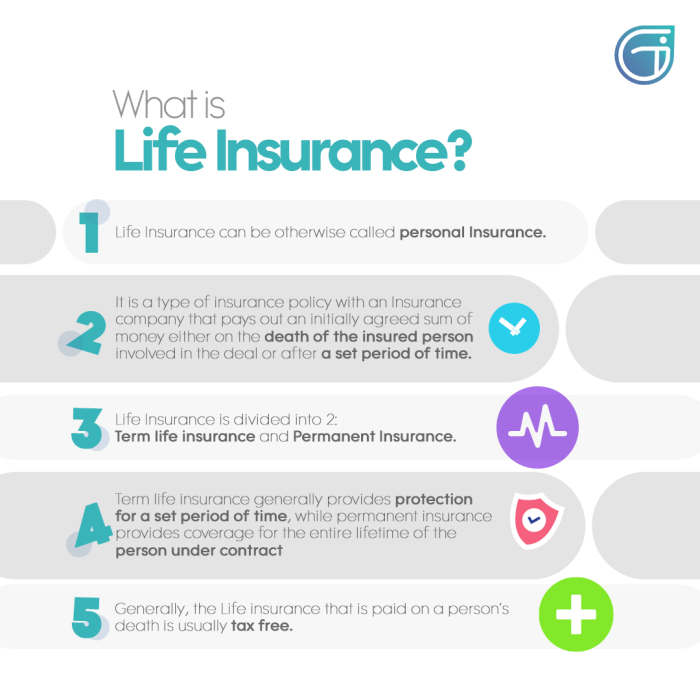

My dear seekers of knowledge, understanding life insurance replacement in Florida is crucial for making informed financial decisions. This intricate process, often driven by evolving needs and circumstances, involves replacing an existing life insurance policy with a new one. It’s a delicate dance between preserving financial security and optimizing coverage, and we shall explore its nuances together.

Precise Definition in Florida Context

Life insurance replacement in Florida signifies the act of terminating a current life insurance policy and simultaneously acquiring a new one. This exchange often aims to enhance coverage, adjust premiums, or change policy features to better align with current financial goals. Crucially, this replacement must comply with Florida’s legal and regulatory framework to ensure fairness and transparency.

Legal and Regulatory Framework

Florida’s regulatory framework, established through statutes and regulations, governs life insurance replacement transactions. These regulations, primarily focused on consumer protection, aim to ensure that replacements are made in a transparent and informed manner. The state’s regulatory body actively monitors these transactions to prevent potential abuses. Agents and insurers are obligated to comply with these regulations to maintain the integrity of the financial system.

Common Scenarios for Replacement

Life insurance replacement is a common response to shifts in financial circumstances. For instance, a family’s needs may evolve, requiring a policy adjustment. A policyholder might seek better premium rates or enhanced coverage amounts. Changes in employment status, investment opportunities, or personal circumstances often motivate such replacements. Additionally, a policyholder might choose a different insurer for a better fit or a more attractive policy structure.

Distinction from Other Financial Transactions

Life insurance replacement is distinct from other financial transactions, such as policy loans or surrenders. A policy loan allows a policyholder to borrow against the cash value of their policy, while a surrender involves the termination of a policy for a partial payout. These differ from replacement, which focuses on acquiring a new policy in place of an existing one.

Understanding these distinctions is vital for navigating these financial decisions with clarity.

Key Players in a Florida Replacement Transaction

The life insurance replacement process involves several key players. The insurer, offering the new policy, plays a crucial role. The insurance agent, acting as a facilitator, assists the policyholder in navigating the complexities of the replacement. Finally, the consumer, the policyholder, makes the ultimate decision about the replacement, based on their needs and circumstances. Their careful consideration is vital for a smooth and beneficial outcome.

Table: Types of Life Insurance Replacement

| Type of Replacement | Description | Florida Statute(s) Involved |

|---|---|---|

| Policy Conversion | Switching from one type of policy to another within the same insurer. | Florida Statutes related to specific policy types. |

| Policy Change | Modifying existing policy terms, such as coverage amount or premium payments. | Florida Statutes related to policy modifications. |

| Policy Exchange | Trading one policy with another from a different insurer. | Florida Statutes related to insurance transactions. |

Types of Life Insurance Replacement

My dear readers, replacing a life insurance policy is a significant decision, often driven by evolving circumstances. Understanding the different types of replacement options available in Florida is crucial for making an informed choice. This discussion will illuminate the various factors influencing this process, providing you with a comprehensive understanding of the landscape.

Different Types of Life Insurance Replacement Products

Florida offers a spectrum of life insurance replacement options, catering to diverse needs and financial situations. These options range from simple term life insurance to more complex whole life policies. The choice depends on the individual’s financial goals, risk tolerance, and future needs.

So, like, Florida’s definition of life insurance replacement is basically when you swap out one policy for another, right? It’s all about finding the perfect fit for your needs, and honestly, checking out homes for sale in Connestee Falls, NC here could totally inspire you to revamp your whole financial game plan. But yeah, back to the insurance thing, it’s all about making sure you’re covered properly, you know?

Term Life Insurance Replacement vs. Whole Life Insurance Replacement

Term life insurance, typically offering a fixed coverage period, is often replaced with another term policy or a permanent policy like whole life, if the initial term is expiring or if the coverage needs have changed. Whole life insurance, with its cash value component and lifetime coverage, might be replaced by another whole life policy with enhanced features or by a different type of permanent policy, like universal life, depending on the policyholder’s financial needs and goals.

The key distinction lies in the coverage duration and the inclusion of a cash value component. A critical aspect is understanding the financial implications of each choice.

Replacing a Policy with a Similar or Significantly Different Policy

Replacing a policy with a similar one, such as exchanging one term policy for another, is often simpler, requiring less paperwork and quicker processing. However, the comparison of benefits, premiums, and coverage is essential. Replacing with a significantly different policy, such as switching from term to whole life, necessitates a more comprehensive assessment, taking into account the long-term financial implications.

This involves a careful evaluation of the cash value component, premium structures, and rider options.

Motivations Behind Replacing a Policy

Individuals might choose to replace a life insurance policy due to various reasons. Changes in financial circumstances, such as a rise in income or a significant life event, often necessitate adjustments in coverage. A policy lapse, due to financial hardship or a change in personal needs, may also motivate a replacement. Furthermore, riders or policy provisions that no longer serve the individual’s needs may be another factor.

Impact of Policy Features on the Replacement Process

Policy features like death benefits, premiums, and riders directly influence the replacement process. A higher death benefit might necessitate a higher premium or more complex policy provisions. The premiums for the new policy need to be evaluated against the current and future financial capabilities of the policyholder. Riders, such as accidental death benefits or critical illness riders, may or may not be available in the replacement policy, impacting the final decision.

Table of Policy Replacement Considerations

| Type of Policy | Key Features | Potential Replacement Considerations |

|---|---|---|

| Term Life Insurance | Fixed coverage period, lower premiums | Expiry of term, need for increased coverage, desire for a cash value component. |

| Whole Life Insurance | Permanent coverage, cash value accumulation | Desire for enhanced features, change in financial circumstances, need for different policy riders. |

| Universal Life Insurance | Flexible premiums, adjustable death benefit | Changing financial needs, desire for greater flexibility in premium payments. |

Consumer Rights and Protections in Florida

My dear seekers of knowledge, understanding your rights in life insurance replacement is paramount. Florida’s laws, with their meticulous care for consumers, provide a safety net to ensure fair dealings in such transactions. This section will delve into the consumer protections afforded, the prohibited practices, and the resources available to you.Florida recognizes the delicate nature of life insurance decisions and aims to protect consumers from unscrupulous practices.

These protections are designed to empower you, the policyholder, to make informed choices without undue pressure or misinformation.

Consumer Rights Related to Life Insurance Replacement in Florida

Florida’s statutes meticulously Artikel the rights afforded to consumers when considering life insurance replacement. These rights are designed to empower you to make sound decisions, free from coercion or misleading information. These rights ensure you have the necessary information and the ability to weigh the pros and cons of a replacement policy.

Consumer Protections Afforded by Florida Law

Florida law safeguards consumers by requiring insurers to adhere to strict standards during replacement transactions. These regulations include mandated disclosures, providing detailed information about the existing and proposed policies. This transparency empowers consumers to compare and contrast policies. Moreover, these protections aim to prevent undue influence or pressure, allowing for well-informed choices.

Examples of Prohibited Practices in Life Insurance Replacement Transactions, What is florida definition of life insurance replacement

Florida law explicitly prohibits certain practices that could potentially harm consumers. These include, but are not limited to, misrepresenting the benefits of a new policy, pressuring consumers into making a decision without adequate time for consideration, and failing to disclose material facts about the existing policy or the proposed replacement. These practices are meticulously Artikeld in Florida statutes, ensuring fair treatment for all involved.

Important Documents to Review During a Replacement Process

Thorough review of critical documents is essential during the replacement process. These include the existing policy documents, the proposed replacement policy documents, and any relevant financial statements or disclosures. These documents provide vital information for comparison and informed decision-making. Comprehending these details is crucial for a successful transition. Furthermore, a thorough understanding of your existing policy will help you make an informed choice.

Role of the Florida Office of Insurance Regulation in Consumer Protection

The Florida Office of Insurance Regulation (OIR) plays a pivotal role in safeguarding consumers in life insurance replacement transactions. The OIR actively monitors compliance with Florida statutes, investigates consumer complaints, and educates the public on their rights and responsibilities. This agency acts as a vital check and balance, ensuring fairness and transparency in the insurance industry. They provide a valuable resource for consumers seeking guidance and support.

Consumer Rights, Responsibilities, and Resources

| Consumer Rights | Consumer Responsibilities | Available Resources |

|---|---|---|

| Right to receive complete and accurate information about the existing and proposed policies. | Carefully review all policy documents and disclosures. | Florida Office of Insurance Regulation (OIR) website, consumer complaint forms. |

| Right to sufficient time to consider the replacement options. | Seek clarification on any uncertainties regarding the proposed replacement policy. | Local consumer protection agencies, legal counsel. |

| Right to be free from undue pressure or coercion during the replacement process. | Ask questions and seek independent advice when necessary. | Insurance professionals with a proven history of ethical practices. |

Agent Responsibilities and Ethical Considerations

My dear seekers of knowledge, let us delve into the crucial responsibilities and ethical considerations that guide life insurance agents in Florida when handling replacement transactions. Understanding these principles is paramount to ensuring fair and transparent practices that protect the best interests of policyholders. A life insurance agent, acting as a trusted advisor, must be mindful of the potential complexities and navigate them with integrity and respect.Agents in Florida, when involved in life insurance replacement transactions, bear a weighty responsibility to act with utmost care and professionalism.

This encompasses a comprehensive understanding of Florida’s specific regulations surrounding replacements, ensuring full disclosure, and meticulously documenting all aspects of the transaction. Ethical considerations are paramount, as agents are obligated to prioritize their clients’ well-being over personal gain.

Agent Duties Regarding Replacement Transactions

Agents play a critical role in the life insurance replacement process, acting as intermediaries between the policyholder and the new insurer. Their responsibilities are multifaceted and require meticulous attention to detail and ethical considerations. They must ensure the policyholder fully comprehends the implications of the replacement, including potential benefits and drawbacks. Accurate and comprehensive disclosure is paramount.

Ethical Considerations for Agents

Ethical conduct is paramount in life insurance replacement transactions. Agents must avoid conflicts of interest and prioritize the policyholder’s best interests above personal gain. This includes recognizing potential conflicts that might arise and taking proactive steps to mitigate them. Their role transcends a mere transaction; it involves fostering trust and providing sound financial advice.

Disclosure and Documentation Requirements

Thorough disclosure and meticulous documentation are essential components of ethical life insurance replacement transactions. Agents must clearly articulate the terms and conditions of the new policy, outlining potential benefits, risks, and costs. This includes any fees or commissions involved, as well as the potential impact on existing benefits and coverage. Maintaining detailed records is vital for demonstrating compliance and accountability.

Importance of Full Disclosure and Client Understanding

Full disclosure is the cornerstone of ethical conduct in life insurance replacement transactions. Agents must ensure the policyholder fully understands the implications of the replacement, including potential tax consequences, changes in coverage, and the impact on their overall financial plan. Effective communication fosters transparency and trust, building a strong foundation for a mutually beneficial agreement.

Potential Conflicts of Interest

Agents must be vigilant in identifying potential conflicts of interest that might arise during replacement transactions. These could include financial incentives that might sway their judgment toward a particular policy or insurer. Understanding these potential conflicts and mitigating them through transparent disclosure and unbiased advice is crucial to upholding the highest ethical standards.

Table: Agent Duties, Actions, and Consequences

| Agent Duty | Example of Action | Potential Consequences |

|---|---|---|

| Full Disclosure | Clearly explaining the terms and conditions of the new policy, including any commissions or fees, to the policyholder. | Failure to disclose material information can lead to legal repercussions and damage the agent’s reputation. |

| Client Understanding | Using clear and concise language to explain complex policy terms and ensuring the policyholder understands the implications of the replacement. | Lack of client understanding can lead to disputes and dissatisfaction, potentially harming the agent’s relationship with the client. |

| Avoiding Conflicts of Interest | Declining to represent a new insurer if a personal financial interest could influence the recommendation. | Failing to address conflicts of interest could result in disciplinary action from regulatory bodies. |

| Maintaining Accurate Records | Creating detailed records of all communications, disclosures, and decisions made during the replacement process. | Insufficient or inaccurate records can complicate compliance and create ambiguity in the transaction. |

Illustrative Examples of Life Insurance Replacement

My dear readers, understanding the intricacies of life insurance replacement in Florida is crucial for making informed decisions. This process, while sometimes necessary, requires careful consideration and adherence to the state’s regulations. Let us delve into illustrative examples to illuminate the steps and potential outcomes.Replacing a life insurance policy is not a simple transaction. It involves a careful evaluation of your current needs and financial goals, along with a thorough understanding of the Florida statutes governing such replacements.

This section will explore a hypothetical scenario, highlighting the steps, disclosures, and consumer rights involved.

Hypothetical Consumer Scenario

A Florida resident, Mr. Ahmed, has a term life insurance policy that he feels no longer adequately covers his family’s needs. His income has increased, and his family has grown. He seeks to replace his current policy with a permanent life insurance policy providing greater coverage and cash value benefits.

Steps Involved in the Replacement Process

The replacement process typically involves several crucial steps. First, Mr. Ahmed consults with a licensed life insurance agent in Florida. Next, the agent will conduct a needs analysis to determine Mr. Ahmed’s current insurance needs and the suitability of the proposed replacement policy.

Crucially, the agent must provide complete and accurate information about the replacement policy, including its features, costs, and potential risks.

Required Disclosures and Documentation

Under Florida law, the agent must provide Mr. Ahmed with a complete disclosure document, known as the Replacement Disclosure Document. This document will detail the policy’s features, costs, and any potential tax implications. Mr. Ahmed will be required to complete a questionnaire and provide relevant financial information to assist the agent in determining the appropriate replacement policy.

Proper documentation of all transactions is essential for compliance with Florida’s regulations. This includes signed consent forms, copies of the old policy, and other supporting documents.

Importance of Consumer Understanding and Consent

Mr. Ahmed must carefully review all disclosures and understand the implications of the replacement transaction. His consent must be freely given, without undue influence or pressure from the agent. This ensures that the replacement decision aligns with his best interests. Informed consent is a cornerstone of the process, ensuring the consumer is not misled.

So, like, Florida’s definition of life insurance replacement? Basically, it’s when you swap out an old policy for a new one, right? But, you gotta check out Johnson & Johnson’s insurance rating ( johnson and johnson insurance rating ) first. It’s all about finding the best fit for your needs, and that’s totally key for the whole replacement process.

Gotta make sure it’s legit, you know?

How Florida Regulations Affect the Replacement Process

Florida statutes require specific disclosures and documentation to ensure consumers are aware of the potential benefits and risks associated with replacing their existing life insurance policies. These regulations aim to protect consumers from potentially harmful or unsuitable replacements. The agent must comply with these regulations to maintain their license.

Potential Outcomes of the Replacement Transaction

The outcome of the replacement transaction can vary greatly depending on Mr. Ahmed’s circumstances and the choices he makes. A successful replacement can provide enhanced coverage and financial security for his family. Conversely, a poorly executed replacement could lead to higher premiums, reduced benefits, or other unintended consequences.

Detailed Example

Replacing a life insurance policy in Florida involves careful consideration and meticulous adherence to the state’s regulations. Mr. Ahmed’s replacement of his term policy with a permanent policy, for example, requires thorough understanding of the proposed changes. The agent must fully disclose the policy’s features, costs, and potential risks. Mr. Ahmed’s informed consent is paramount. Failing to comply with these regulations could lead to negative financial implications.

Final Conclusion

In conclusion, navigating Florida’s life insurance replacement landscape requires a deep understanding of the legal framework, consumer rights, and agent responsibilities. This guide provides a structured overview of the process, highlighting the importance of informed decision-making and full disclosure. By understanding the potential financial implications and seeking professional advice when needed, consumers can make choices that align with their financial goals and circumstances.

Query Resolution

What are some common scenarios where life insurance replacement might be considered?

Common scenarios include changing financial needs, policy lapses, or a desire to improve coverage. A need for a different type of policy (e.g., term to whole life) or a more favorable policy structure might also trigger a replacement.

What are the key distinctions between life insurance replacement and other financial transactions?

Replacement transactions involve specific legal and regulatory requirements regarding disclosure, consumer protection, and agent responsibilities, which set it apart from other financial transactions.

What is the role of the Florida Office of Insurance Regulation in consumer protection?

The Florida Office of Insurance Regulation plays a crucial role in ensuring that replacement transactions are conducted fairly and transparently, upholding consumer rights and protecting them from potential abuses.

What documents should consumers review during a life insurance replacement process?

Consumers should review the policy’s terms and conditions, disclosure documents provided by the agent, and any related regulatory information provided by the Florida Office of Insurance Regulation. Understanding the details of the new policy is critical.